If you are a current FCI client, Schedule your Consult Online or call (617) 500 7410

Posted in Cloud Computing, Tech Sales Institute, tagged . Check Point Software, Aruba, Avaya, Blue Coat Systems, Brocade, CISCO, Cloud Computing, CSCO, EMC, Enterprise Tech Infrastructure, F5, F5 Networks, Fizz, Fortinet, GOGRID, HPQ, Michael Horsch Fizz, NetApp, Rackspace, RIVERBED, ruckus, SDN NFV, SWOT Review - Strength / Weakness / Opportunity / Threat, Tech Sales Institute, Technology Market Trends and Outlook on August 6, 2014|

If you are a current FCI client, Schedule your Consult Online or call (617) 500 7410

Posted in Cloud Computing, Tech Sales Institute, tagged . Check Point Software, Aruba Networks, Avaya, Blue Coat Systems, BMC Software, CISCO, Cloud Computing, CSCO, EMC Corporation, Enterprise Tech Infrastructure, F5, HP, IBM, Juniper, Juniper Networks, Michael Horsch Fizz, NetApp, Oracle, PaaS, RIVERBED, SDN NFV, SWOT, SWOT Review - Strength / Weakness / Opportunity / Threat, Tech Sales Institute, Tech Sales jobs, Technology Market Trends and Outlook, Uncategorized, verizon on February 19, 2014|

AVAILABLE 02/21/2014 for current FCI and GLG Clients. Limited Time Slots Schedule your consult now!

FCI Clients: Schedule your consult directly with Michael

GLG Clients: Schedule your consult with GLG

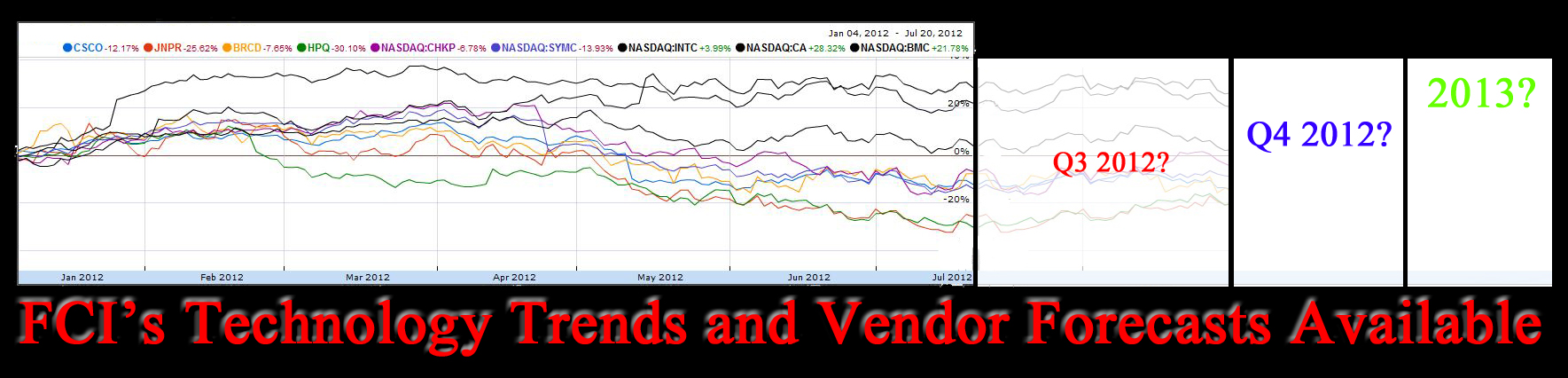

Posted in Cloud Computing, tagged . Check Point Software, Avaya, CISCO, Cloud Computing, Enterprise Tech Infrastructure, HP, HPQ, Michael Horsch Fizz, RIVERBED, SWOT, Tech Sales Institute, Technology Market Trends and Outlook on July 25, 2013| 1 Comment »

FCI and GLG clients may schedule consults now to review Tech Spending performance and trends.

Posted in Uncategorized, tagged Avaya, CISCO, Dell, F5 Networks, HP, IBM, Juniper Networks, Meru, Oracle, RIVERBED, ruckus, Uncategorized on February 12, 2013| Leave a Comment »

We see sequential Qrt over Qrt growth for Q2 2013 strongest since 2011. FCI clients can schedule consults now to review with Michael.

Posted in Cloud Computing, tagged Aruba, Avaya, Brocade, Checkpoint, CISCO, Cloud Computing, EMC Corporation, Enterprise Tech Infrastructure, F5, Fizz, GOGRID, HP, IBM, Juniper, Meru, NetApp, Oracle, PaaS, Rackspace, RIVERBED, ruckus, Symantec, Technology Market Trends and Outlook on November 21, 2012| Leave a Comment »

Our latest enterprise tech spending data is clear. Steady tech spending continued in November. It does fluctuate by vertical, tech niche and vendor. However, overall we are in a very good position for closing the fourth quarter. Storage, App optimization, Security, Networking, Wireless LAN — lead with an est 4 – 6% Qrt over Qrt growth. Servers flat. Vendor performance and tech niche details available.

11/21/2012 VAR/SI poll shows the majority are ill prepared for selling IaaS, PaaS, SECaaS, BIaaS, in the medium to large business sectors. With an important exception. VAR’s/SI’s with a committed and proven acumen for selling vertical specific infrastructure solutions and/or vertical application solutions ARE succeeding in selling Cloud solutions. FCI/GLG clients: Set up a consult to review.

Happy Thanksgiving,

Michael Horsch Fizz

Principal Advisor

Posted in Uncategorized, tagged AMAZON, Avaya, Brocade, Checkpoint, CISCO, Fortinet, GOGRID, Iaas, IBM, Infrastructure, Intel, Michael Horsch Fizz, NetMotion, Oracle, PaaS, Palo Alto, Rachspace, Romley, Technology Spending Forecast, Trends, Uncategorized, Wireless on July 21, 2012| Leave a Comment »

Posted in Cloud Computing, tagged . Check Point Software, 3PAR, Avaya, Blue Coat Systems, BMC Software, Brocade, CA, CISCO, Citrix, Cloud Computing, Double-Take Software, EMC Corporation, Emulex Corporation, Enterasys, Extreme Networks, F5 Networks, FalconStor Software... Hitachi, Inc McAfee, Inc., Inc. NetApp Inc. Oracle Corporation Sun Microsystems Overland Storage, Inc. NetGear, Inc. QLogic Corporation Quantum Corporation Radware Ltd. Riverbed Technology... SonicWALL, Inc. Sourcefire, Inc. Symantec Corporation Trend Micro Inc. (ADR) VMware, Inc. Websense Inc. 0 0 0 Polycom Tandberg (Cisco) Radvision NetScout solarwinds redhat fortinet, Joyent, Ltd. (ADR) Hewlett-Packard Company Intl. Business Machines… Juniper Networks, NaviSite, PaaS, Rackspace, RIVERBED, Technology Market Trends and Outlook, Terramark, verizon on September 26, 2011| Leave a Comment »

The IT spending forecasts we provide are up to three months ahead of actuals and up to four months ahead of realized market changes. Q3 2011 will see slight shrinkage in IT spending for the large enterprise space. Preliminary Q4 2011 numbers show the pipeline will deliver somewhere in the mid single digest for Qrt over Qrt growth. Our final forecast numbers and actuals will be available by October Fifth, 2011. The financial vertical is finally stable again however will most likely NOT make up for the delta in Q4. Health care, health care insurance and bio/pharm continues to give us consistent growth.

Detailed reviews available through GLG.

From the SI perspective we can review the strengths, challenges, competitor comparisons, client demand and future outlook. Through GLG we can provide estimated vendor performance as seen through our present and expected technology reviews.

In addition we can share how present economic conditions have effected to the positive or negative spending trends for specific technologies as well as a macro review of spending trends.

Michael Horsch Fizz

Principal Advisor

FCI

LinkedIn: http://www.linkedin.com/in/fitceo

News: http://michaelfizz.com/

MHF