AVAILABLE 02/21/2014 for current FCI and GLG Clients. Limited Time Slots Schedule your consult now!

FCI Clients: Schedule your consult directly with Michael

GLG Clients: Schedule your consult with GLG

Posted in Cloud Computing, Tech Sales Institute, tagged . Check Point Software, Aruba Networks, Avaya, Blue Coat Systems, BMC Software, CISCO, Cloud Computing, CSCO, EMC Corporation, Enterprise Tech Infrastructure, F5, HP, IBM, Juniper, Juniper Networks, Michael Horsch Fizz, NetApp, Oracle, PaaS, RIVERBED, SDN NFV, SWOT, SWOT Review - Strength / Weakness / Opportunity / Threat, Tech Sales Institute, Tech Sales jobs, Technology Market Trends and Outlook, Uncategorized, verizon on February 19, 2014|

AVAILABLE 02/21/2014 for current FCI and GLG Clients. Limited Time Slots Schedule your consult now!

FCI Clients: Schedule your consult directly with Michael

GLG Clients: Schedule your consult with GLG

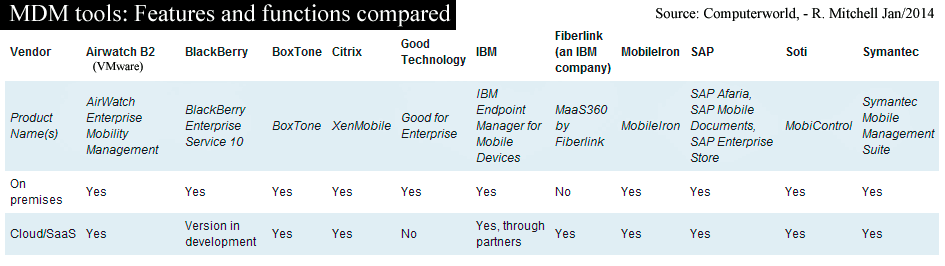

Posted in Cloud Computing, Tech Sales Institute, tagged acquisition, AT&T, Check Point, CISCO, Cloud Computing, Enterprise Tech Infrastructure, Good Technology, HP, IBM, Juniper, MDM, Mergers, Mobile, Tech Sales Institute, Tech Sales jobs, Technology Market Trends and Outlook, verizon on February 6, 2014|

Established Security and Networking Vendors DESPERATELY looking to stabilize and increase market share should hunt for partners and vendors in the following categories:

Based on current trends and expected demand I expect aggregate Year over Year growth for the above categories to reach 25%+ in 2014.

With VMware scooping up AirWatch, what is the probability Cisco, Juniper, HP, Check Point and others will add or improve via M&A. Stay tuned!

For established Integrators, Mobile Security and MDM is lucrative. Not sure who to partner with? Schedule a consult to review.

– Michael Horsch Fizz, Principal Advisor

MDM Vendors 2014

Posted in Cloud Computing, tagged . Check Point Software, 3PAR, Avaya, Blue Coat Systems, BMC Software, Brocade, CA, CISCO, Citrix, Cloud Computing, Double-Take Software, EMC Corporation, Emulex Corporation, Enterasys, Extreme Networks, F5 Networks, FalconStor Software... Hitachi, Inc McAfee, Inc., Inc. NetApp Inc. Oracle Corporation Sun Microsystems Overland Storage, Inc. NetGear, Inc. QLogic Corporation Quantum Corporation Radware Ltd. Riverbed Technology... SonicWALL, Inc. Sourcefire, Inc. Symantec Corporation Trend Micro Inc. (ADR) VMware, Inc. Websense Inc. 0 0 0 Polycom Tandberg (Cisco) Radvision NetScout solarwinds redhat fortinet, Joyent, Ltd. (ADR) Hewlett-Packard Company Intl. Business Machines… Juniper Networks, NaviSite, PaaS, Rackspace, RIVERBED, Technology Market Trends and Outlook, Terramark, verizon on September 26, 2011| Leave a Comment »

The IT spending forecasts we provide are up to three months ahead of actuals and up to four months ahead of realized market changes. Q3 2011 will see slight shrinkage in IT spending for the large enterprise space. Preliminary Q4 2011 numbers show the pipeline will deliver somewhere in the mid single digest for Qrt over Qrt growth. Our final forecast numbers and actuals will be available by October Fifth, 2011. The financial vertical is finally stable again however will most likely NOT make up for the delta in Q4. Health care, health care insurance and bio/pharm continues to give us consistent growth.

Detailed reviews available through GLG.

From the SI perspective we can review the strengths, challenges, competitor comparisons, client demand and future outlook. Through GLG we can provide estimated vendor performance as seen through our present and expected technology reviews.

In addition we can share how present economic conditions have effected to the positive or negative spending trends for specific technologies as well as a macro review of spending trends.

Michael Horsch Fizz

Principal Advisor

FCI

LinkedIn: http://www.linkedin.com/in/fitceo

News: http://michaelfizz.com/

Posted in Cloud Computing, tagged AMAZON, API, CISCO, Cloud Computing, CSC, CSP, Datapipe, EC2, F5, Fizz, GOGRID, GOOGLE, hosting.com, Iaas, IBM, Joyent, NaviSite, OpSource, PaaS, Rackspace, RIVERBED, Savvis, Technology Market Trends and Outlook, Terramark, Uncategorized, verizon on May 12, 2011| 1 Comment »

Asked by John Demarchi, Director, Emerging & Social Media, Gerson Lehrman Group at GLGPLUS.

ANSWER:

The following list will change quickly. Why? Because we are in a hurricane of old, new, and reinvented cloud providers. In addition, I focus on the enterprise space and as a result the Cloud Service Providers (CSP’s) are reviewed through enterprise technology lenses. Some have my personal view, opinion, thoughts attached and do not necessarily reflect the views, opinions, or thoughts of my clients or any other entity.

Not in any specific order.

Amazon – http://aws.amazon.com/vpc/ http://aws.amazon.com/ec2/

Amazon Web Services (AWS). Despite the major hickup recently with Amazon’s Elastic Cloud (EC2) they will continue to make strides. Due to their recent intrinsic investments aimed at dramatically improving their support services it will most likely make them a stronger contender in the enterprise space.

However, since I focus primarily on the large enterprise my greatest interest is for their beta service called Amazon Virtual Private Cloud (Amazon VPC). My sensors are tuned to monitor their progress. If done correctly they will hit it into the higher elevations of the troposphere and may even be one of the few cloud service providers edging into the stratosphere.

============

GoGrid – http://www.gogrid.com/cloud-hosting/

“pure-play Infrastructure-as-a-Service (IaaS) provider specializing in Cloud Infrastructure solutions. ” They claim over 10k of clients.

============

NaviSite – http://www.navisite.com/technology-navicloud-platform-architecture.htm

Time Warner Cable now owns NaviSite (April 2011) My experience with NaviSite has been a very positive one for many years. What I like most is their offer to the enterprise client. While some CSP’s focus on SMB and re- architect (maybe) for the enterprise space, NaviSite’s services are built for the enterprise. My concern is with Time Warner Cable. The monetary benefits they bring to the table means little if they change for the negative the culture and front line intellectual assets of NaviSite. We shall see.

============

CSC – http://www.csc.com/cloud/

The fifty year old CSC has a plethora of cloud initiatives. CSC has traditionally been low on the ground staying to the topology of traditional infrastructures. However, they are very quickly shooting into the troposphere with a plethora of cloud services. The two most important today are SmartStart and BizCloud. “CSC Smart Start is a hands-on proof-of-concept (PoC) program that lets you test drive the cloud, minimize risk and avoid capital investments — even for an on- premises private cloud — while discovering the benefits of the cloud.” BizCloud addresses the sweet spot for the larger enterprise space. CSC has launched a private cloud service called BizCloud. The company leverages VCE the packaged cloud solution from VMware, Cisco and EMC. “CSC BizCloud is a private cloud, billed as a service from a standard rate card and ready for workloads in just 10 weeks. With BizCloud you get the security and exclusivity of a private cloud with all the economic advantages and convenience of the public or leveraged cloud infrastructure.”Once running it can even sync into CSC public cloud offering also running on VCE.

CSC gets it when it comes to understanding the interest, demand and requirements of their clients. Sweet spot may very well be right below the large enterprise space.

============

NephoScale – http://www.nephoscale.com/

Cloud startup building out its own data center and selling on demand similar to Amazon Web Services or Rackspace.

============

Joyent – http://www.joyent.com/

With their latest platform software Joyent remains in the running. Their partnership with Dell to sell pre-configured cloud infrastructure packages is a great opportunity however history would tell us Dell may not be the best infrastructure partner in the enterprise space. Joyent empowers their clients to build out a private cloud OR use Joyent’s public cloud services.

============

Microsoft – Azure and Office 365

MS’s Azure in the PaaS category has strongly marketed Azure. They claim more than 30k clients. Some success with mobile companies and web companies. However, in the large enterprise space where we work we have not experienced any significant traction. They have also finally made available Office365 which falls into the SaaS space. Two categories, 1) 25 users and under which pay monthly or 2) 25 users or more which pay yearly. For the long-term success of MS’s Office they MUST make this a profitable initiative.

Also keep in mind their top management has been turned upside down and/or out. Ozzie (SW), Muglia (Azure), and Thompson (O365) are all vapor.

Azure – http://www.microsoft.com/en-us/cloud/developer/default.aspx?fbid=NbMJRe-RbjK

Office 365 – http://www.microsoft.com/en-us/office365/online-software.aspx

============

BlueLock – http://www.bluelock.com/bluelock-cloud-hosting/vcloud-datacenter/

BlueLock comes to us via VMware’s vCloud. We have been impressed with how they enable new entrants with Bluelock’s CloudStart Program. From independent reviews their cloud architecture is secure and reliable. Their dependence on VMware is of course a variable to keep a close eye on.

============

Google –

Google and their Google App Engine – http://googleappengine.blogspot.com/ has hit the ball out of the park with web providers, gaming developers and mobile providers. Their enterprise initiatives have not garnered great results. However, recently they have hired numerous foot soldiers. If their recruitment continues it will soon become a large division to tackle the needs and concerns of developers in the large enterprise space.

============

Rackspace –

Rackspace is the long-standing rival of Amazon continues to add new clients. They needed a couple of differentiators and they now have them. The first is a cloud OS called Openstack http://www.rackspace.com/cloudbuilders/openstack/

The second is Cloudkick http://www.rackspace.com/cloud/tools/applications/cloud-servers-partners/system-management/cloudkick/ enabling web-based management tools required by larger enterprise clients.

============

Salesforce – http://www.salesforce.com/platform/

Salesforce has always been on top when it comes to Software as a Service (SaaS). Now they are marching with might into Platform as a Service (PaaS). This was mostly due to their acquisition of Heroku. http://www.heroku.com/ In addition, they are continuing with Force.com. A leading cloud platform for business apps that includes Appforce, SiteForce, VMforce, ISVforce all open standards based API.

============

IBM – http://www.ibm.com/cloud-computing/us/en/

IBM is finally getting their act together. Well, at least on the front lines when it comes to packaging, repackaging and offering vertical specific cloud solutions as well as general IaaS, PaaS and SaaS solutions. However, what I am keeping a closer eye on is their cloud go to market strategy with Ingram Micro. Why? In North America alone we have thousands of VAR’s and Systems Integrators trying to figure out what their next chapter will look like. The cloud providers that offer them the most lucrative and sustainable agreement to sling their services will gain exponential representation in the market. Just ask Cisco the value of simply out representing the competition. Of course the greatest opportunity for the VAR’s and SI’s continues to enabling their existing and future clients to make the transition from traditional IT operations to cloud centric operations regardless of the flavor.

============

Oracle – http://cloud.com/products/cloud-computing-software

Oracle potentially has it all. The core infrastructure (minus the network), the middleware, the database, the application, open source and JAVA, – As an old Sunster I was hoping they would be further along when compared to some of the other bigger players such as IBM.

============

Verizon – http://www.terremark.com/services/cloudcomputing.aspx

Verizon bought Terremark. I like(d) Terremark. They have success under their belt in the enterprise cloud space. AND, my head is still trying to assimilate April 2011 milestone of Verizon’s acquisition of Terremark. Time will tell.

============

Datapipe – http://www.datapipe.com/solutions-cloud-computing.htm

Managed Services abutted and entwined into Amazon EC2 – simply an extension/addition to an Amazon EC2 solution

============

CA – http://www.ca.com/us/cloud-management-console.aspx

On an acquisition frenzy – we shall see if they can stitch it all together to convince their impressive client base to adopt. The biggest feather in their cap is 3Tera.

============

ENKI – http://www.enki.co/primacloud/

They keep jumping onto my radar with virtual private data centers Primacloud – For me, the jury is out on the company’s management coupled with their ability to scale (in sales and marketing).

============

Enomaly – http://www.enomaly.com/

The rubber band computing provider. Accoring to my peers in the SP space they have an impressive IaaS offering focused on service providers.

============

Eucalyptus – http://www.eucalyptus.com/products/eee

Open Source Software Platform that has proven itself. Private cloud services – their sweet spot may be the government sector. IF the US govt is truly committed to having a private cloud infrastructure by 2012 and if Eucalyptus can penetrate deeper into the govt sector then they could accelerate even faster. A lot of “if’s”. However they have already had success in the large enterprise and are receiving accolades.

============

OpSource – http://www.opsource.net/Solutions

“OpSource provides cloud and managed hosting solutions that enable businesses of all sizes to accelerate growth and scale operations while controlling costs and reducing IT infrastructure support risks. More than four hundred Software- as-a-Service ISVs, cloud platform providers, carriers and enterprises rely on OpSource’s ability, experience and agility to operate high-availability, business-critical hosting environments.”

============

Savvis – http://cloud.savvis.com/

Savvis has more than 30 locations and as a company provides a potpourri of cloud, hosting and network services. What I am most excited about is their push into the DC beltway. Again, if the US govt is serious about its IT architecture shift into the cloud, Savvis gains to win big and have even better traction in the large enterprise as well.

============

Hosting.com – http://www.hosting.com/solutions/compliance

They get it when it comes to the elevated concerns of cloud computing from the financial and medical vertical. Their dedication to making sure they meet and exceed regulatory requirements to assure client compliance is a differentiator.

+++++++++++++

Again, not a complete list. Keep in mind the “buckets” within the cloud, Public, Hybrid, Private, PaaS, SaaS, IaaS. Some of the aforementioned CSP’s fall into only a couple and some fall into all.

In addition, you will want to keep an eye on cloud provider enablers like VMware and their VMware vCloud™ Datacenter Services.

If you are going to “bet” on winners, look at the sure win of infrastructure providers. The network vendors such as Cisco, Juniper, Brocade, are sure wins. In addition, WOC and Load Balancing vendors such as Riverbed (WOC) and F5(Load Balancing) are well positioned. ALL of the aforementioned CSP must have the plumbing in place and the end users must have fast and reliable services. A clear differentiators of cloud providers is their investments in the architecture coupled with predictive and proactive management of their cloud solution.

All for now.

Michael Horsch Fizz

Principal Advisor

FCI

www.fitceo.com

LinkedIn: http://www.linkedin.com/in/fitceo

News: http://michaelfizz.com/

MHF